Over the past few years, TAP Air Portugal had quite the rollercoaster ride. After – like many airlines across the world – being hit hard by the pandemic, and being rescued by its government, with the aid’s approval by the European Commission (EC) being annulled, and later reapproved, the Portuguese carrier is now turning a new chapter, a chapter that will include outside investment.

Following the Portuguese government’s approval, Parpública, the state holding company, invited potential suitors to submit a statement of interest to acquire up to 44.9% of TAP Air Portugal’s shares. Air France-KLM, the International Airlines Group, and Lufthansa Group have confirmed their participation in the process, and The Engine Cowl explores why.

Chaos in Portugal

The sale of the 44.9% stake – the Portuguese state will keep 50.1%, while TAP Air Portugal’s employees will get the remaining 5% – traces its roots back to the pandemic, when in 2020, the Portuguese state granted a €1.2 billion ($1.3 billion) rescue loan for “immediate liquidity needs considering an amount equivalent to the liquidity needs for a 6-month period from July 2020 to December 2020.”

Later, in December 2021, the EC approved another state aid package worth €2.55 billion ($2.9 billion). As part of the whole restructuring process, the Portuguese state became the owner of TAP Air Portugal.

As later argued by the Portuguese government in September 2025, while TAP Air Portugal plays a crucial role in the country’s connectivity, the airline operates in a “competitive and global sector, where business scale is essential for strengthening the network of destinations, passenger service, and improving the efficiency of the entire operation.”

As a result, and with the EC’s decision preventing the Portuguese state from investing more into the airline, “it is crucial to resume the reprivatization of its share capital, by seeking a strategic partner for its operation, which will leverage the company's assets, its brand and its key routes, in compliance with the applicable regulatory framework at the national and European Union [EU] levels.”

Thus, the Portuguese government proceeded with the sale of a minority stake in TAP Air Portugal, and three suitors, namely Air France-KLM, the International Airlines Group (IAG), and Lufthansa Group, have emerged as potential groups to more closely integrate the Portuguese airline within their operations.

Pedro Castro, a Portugal-based air transportation expert and the founder of SkyExpert, an airline consultancy, told The Engine Cowl that even if the EU has mandated Portugal to sell a stake in TAP Air Portugal, the country has one of the “highest numbers of infringement procedures for non-compliance.”

Castro added that the process could become “messy," including politically.

“I just do not know when or how: it could be manifested in day-to-day interference, since we have already seen a minister responsible for TAP Air Portugal openly admitting to reviewing and altering TAP's press releases, in a boardroom by blocking important but politically unpopular decisions, or in a change of government leading to a complete shift in direction of the other shareholder (the State).”

Slots at Lisbon Airport

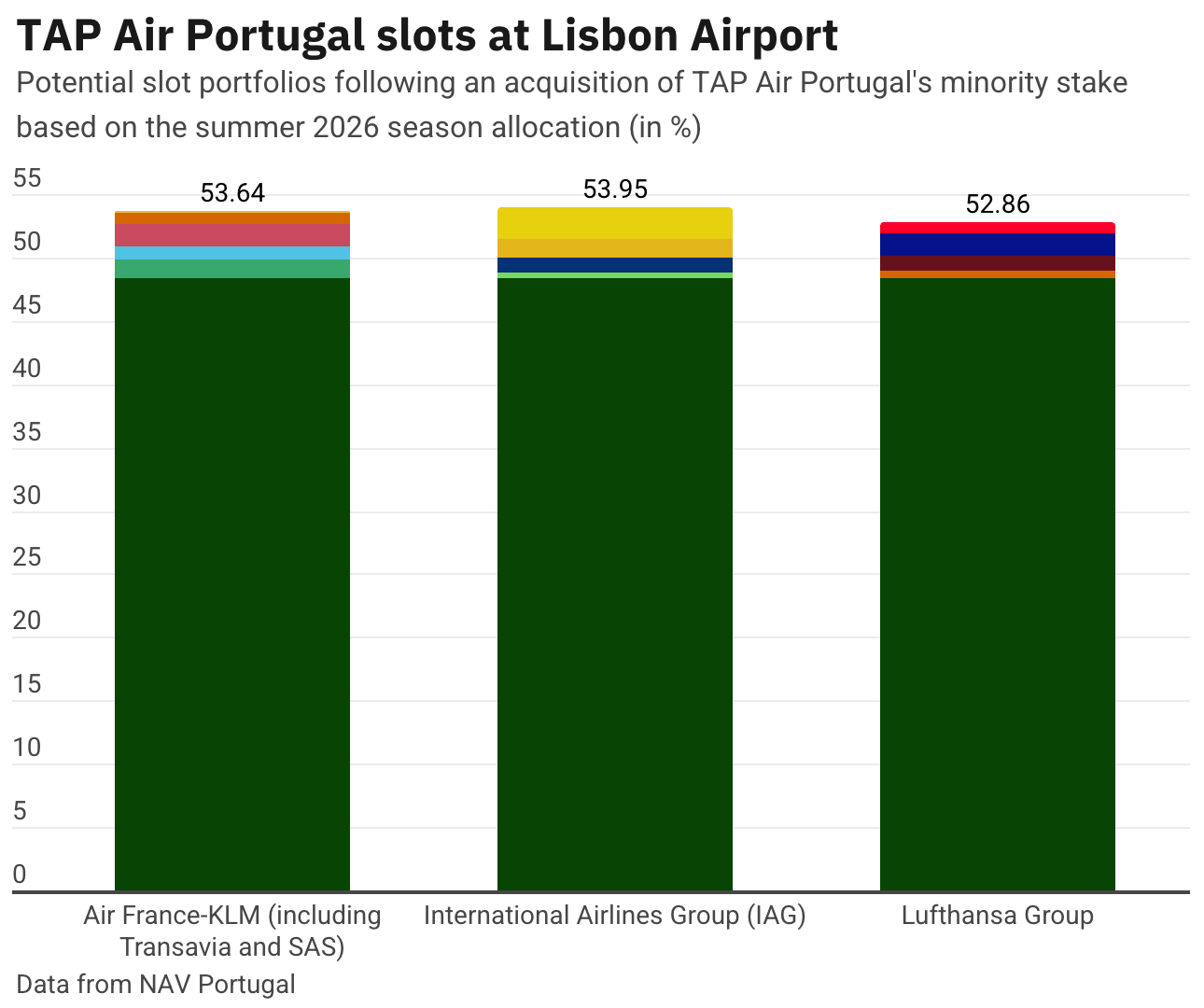

However, TAP Air Portugal has something that many airlines, including, for example, JetBlue, have long wanted: a lot of slots at Lisbon Airport (LIS). According to NAV Portugal, the country’s air navigation services provider (ASNP) and slot coordinator at LIS and other Portuguese airports, TAP Air Portugal controls over 48% of slots at LIS.

Of the 164,615 requested slots, NAV Portugal allocated 146,682 movements to operators for the summer 2026 season. During the summer 2025 season, the Portuguese ASNP initially allocated 146,579 slots to airlines. What would happen with the slot share at LIS if Air France-KLM, IAG, or Lufthansa Group were to become the minority shareholders of TAP Air Portugal?

All three groups, following the acquisition of a minority stake in the airline, would hold around 53% of the total slots at LIS.

(Air France-KLM’s potential slot portfolio includes SAS, whose majority shareholder, barring any regulatory hurdles, should become the Franco-Dutch airline group.)

Castro noted that if slots at LIS are a prized possession right now, “it may only last for one decade, as the government is pushing the agenda for a new mega-airport 40 kilometers [24.8 miles] away from Lisbon.”

“However, no firm decision exists concerning the future of the existing airport, which means the investment scenarios remain unclear.”

The Portuguese national was confident that any new TAP Air Portugal shareholders would have to consider that gaining competition authorities’ approval would include “inevitable remedies” of slots at LIS, and while it is currently unclear how many slots the airline would have to give back to the slot pool, airlines, including from countries that would be interested in the merger, “struggle to obtain proper slots at Lisbon, and this deal represents a one-time opportunity to address that issue.”

Furthermore, when the EC approved Lufthansa Group’s initial investment in ITA Airways, it also examined the potential impact that the tie-up would have not only on European short-haul routes but also on specific long-haul routes between Europe and North America.

In its own words, in its previous decisions, the EC “considered the activities of certain [joint venture] partners of the parties to the transaction in relation to routes covered by joint venture agreements as part of the parties’ activities.”

As such, while TAP Air Portugal is currently a member of Star Alliance, each of the flagship airlines within their groups have extensive JV agreements with carriers, including, for example, the American Airlines, British Airways, Finnair, and Iberia partnership on transatlantic flights.

Castro pointed out that potential remedies “may not only involve generic slot concessions at Lisbon but also very targeted ones involving specific city pairs and other congested airports, such as the ones linking [LIS] to Amsterdam [AMS] or [LIS] to London-Heathrow [LHR].”

“One thing is certain: surrendering Lisbon slots will be necessary for the deal to be approved, and this will significantly impact competition.”

TAP Air’s network

According to Cirium’s Diio Mi, TAP Air Portugal’s weekly departures will peak in July this year, with the airline offering 1,337 weekly flights across its network from LIS and Porto Airport (OPO). One of the major advantages that the Portuguese airline has over its European peers is, one, its Brazilian network.

During the same month, TAP Air Portugal will offer 100 weekly departures from Portugal to Brazil, serving 14 routes and 12 destinations in the South American country. TAP Air Portugal will serve seven destinations in Brazil that are not served by any other airline flying between Europe and Brazil.

Another strong point is Africa, given Portugal’s proximity to the continent, especially its western part.

Castro highlighted that, considering the slot constraints at LIS, he is not “convinced that exporting the traditional hub concept is the most effective way to achieve” higher profit margins for any of the airline groups looking to acquire a minority stake in TAP Air Portugal.

“I believe Lisbon will gain access to new routes and hub destinations depending on which group acquires TAP,” he added, noting that this could include new services to such airports as Dallas/Fort Worth International Airport (DFW) or Hartsfield-Jackson Atlanta International Airport (ATL), where IAG and Air France-KLM’s North American partners have fortress hubs.

“Lisbon will probably continue to serve as a ‘niche hub’ for certain destinations that are either served exclusively from Lisbon or are more profitable from Lisbon due to shorter flight times and existing local traffic.”

At the same time, Castro questioned whether it is worth these groups pursuing transfer traffic at LIS, given the lack of slots at the airport, but did note gaps in TAP Air Portugal’s network, including that the airline does not have any flights to Asian destinations, and that its easternmost destination will be Tel Aviv Ben Gurion International Airport (TLV).

The March 29 restart of its LIS-TLV route could be delayed due to the current situation in the region. OPO-TLV is scheduled to begin on October 25.

While Lufthansa Group will present its annual results on March 6, and IAG’s executives had little to share about TAP Air Portugal during their Q4 2025 earnings call, Air France-KLM’s Chief Financial Officer (CFO), Steven Zaat, told the media following the publication of its Q4 2025 results that “we had a nice conversation […] with [TAP Air Portugal’s] management team, and at the end of the day, it all comes down to what they want to have, what they feel comfortable with, and what are we comfortable with in our joint approach.”

“[…] they can have a central place in our group in terms of group organization, and that was the discussion we had in Lisbon.”

Zaat added that it will be up to TAP Air Portugal to decide on which group to side with, and from Air France-KLM’s perspective, the price of the transaction and the governance structure.

“We are not going to invest in a company in which we have no confidence that they can reach an 8% margin,” Zaat continued, noting that TAP Air Portugal is “a good player in South America, and, of course, being part of the group will make them stronger than they were before.”

Ben Smith, the Chief Executive Officer (CEO) of Air France-KLM, provided more color, saying that TAP Air Portugal’s current network “is very complementary to what we have at the group,” and what the Franco-Dutch group brings is a “more comprehensive coverage of South America.”

If Air France-KLM succeeds in acquiring a stake in TAP Air Portugal, as well as SAS, the airlines will have a much more diversified network across Europe, and provide an overall positive boost to the group’s network.

“Having an entry point into Latin America from the Iberian Peninsula would strategically be great for us.”

IAG’s annual report did affirm that the group is “currently participating in the partial disposal process by the Portuguese government of TAP, which we think is a strategically interesting opportunity for the Group but will have to be on terms that create value for IAG’s shareholders.”

Castro concluded that any potential buyer acquiring a stake in TAP Air Portugal is buying into political uncertainty, since the airline has been a highly politicized subject in the country. The airline has been “frequently used by politicians as their ‘playground’,” he continued, saying that, for example, unlike Lufthansa Group’s acquisition of any of its subsidiaries, “which followed clear roadmaps and guidelines toward full ownership, there is no clear path in the case of TAP Air Portugal.”

“Given Portugal’s political volatility, that uncertainty is part of the airline’s risk profile that investors will need to consider.”