easyJet published its FY2026 H1 (October to March) results on May 21.

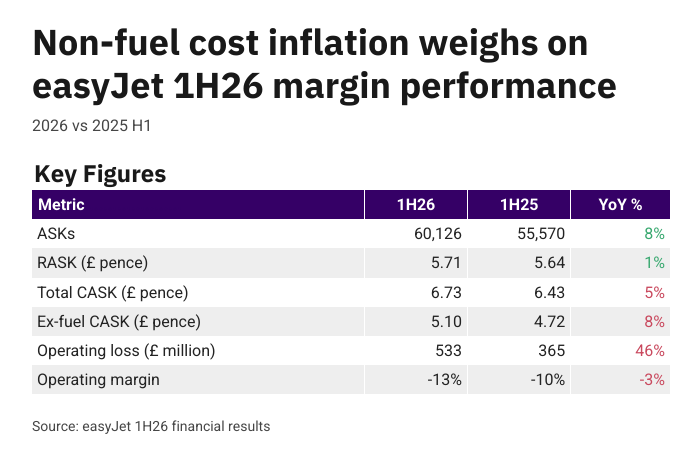

Despite unit revenue growth, higher non-fuel expenses widened the airline’s H1 operating loss from £369 million last year to £533 million in FY26.

Key Figures

Longer stage length driving ASK growth

Capacity measured in available seat kilometers (ASKs) was up 8% year-on-year (YoY), driven partially by a 4% increase in average stage length. easyJet’s winter stage length has been increasing over the past two years and is now 10% higher than it was two years ago as the airline deploys more capacity into longer-stage leisure markets.

Robust revenue performance

Revenue per ASK, which typically moves inversely to stage length, was up 1% compared to last year, partially helped by an earlier Easter in 2026.

In addition to higher fares, the airline also cited revenue growth from higher bundle attach rates, strong demand for the newly-introduced Flex Pass, and improved in-flight retail performance.

Cost inflation weighing on the business

Despite higher fuel spot prices towards the end of the period, it was actually easyJet’s non-fuel expenses which put a damper on performance.

Ex-fuel CASK increased by 8% compared to last year while fuel CASK was actually down 5%.

Almost all non-fuel expenses grew in excess of the airline’s 8% ASK growth. Among the largest non-fuel expenses, airport and ground handling costs increased by 15% YoY, crew costs increased by 21%, and navigation costs were up 17%.

Iran conflict compressing the booking curve

easyJet highlighted that “forward bookings have been impacted by the conflict in the Middle East, resulting in a later booking curve” and that “overall bookings for the summer period are behind where they were at this point last year”.

Load factor is currently booked to 79% for the June quarter, one point behind last year. Booked RASK is down 4%, implying an approximately 3% lower yield which partially reflects more Easter demand falling into the tail-end of H1.

The airline has already implemented a 0.3% capacity reduction for the summer and redeployed capacity from the eastern Mediterranean to shorter domestic and city markets. No further system-level capacity cuts are expected for the summer.

Despite a more challenging environment, easyJet maintains one of the industry’s strongest balance sheets with access to £4.7 billion in liquidity and an impressive £434 million net cash position.

Looking further ahead, easyJet plans to launch a loyalty program in FY27 and expects to retire its 79 A319 aircraft by FY29.