After our round-up of first quarter financial results for the US Big Four last week, The Engine Cowl takes a look at the highlights from the rest of the publicly-traded United States-based airlines.

Key Themes

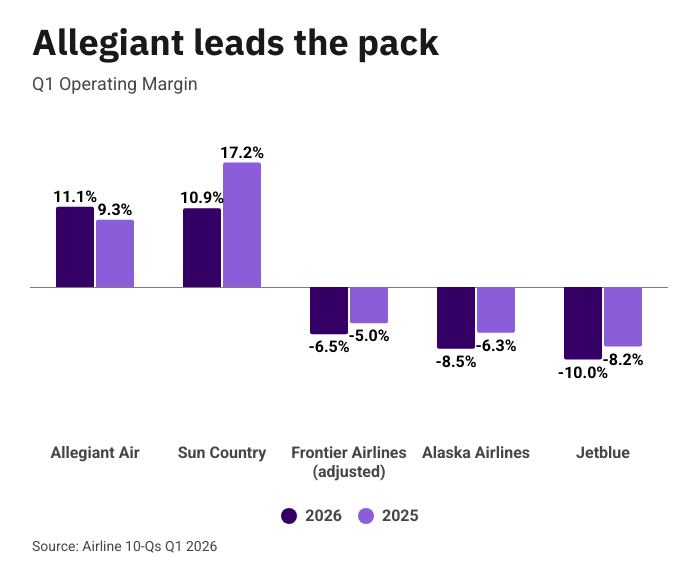

- While operating margins at the Big Four grew compared to last year, performance was less rosy for the mid-size airlines. Four of the five carriers saw operating margins fall compared to 1Q25.

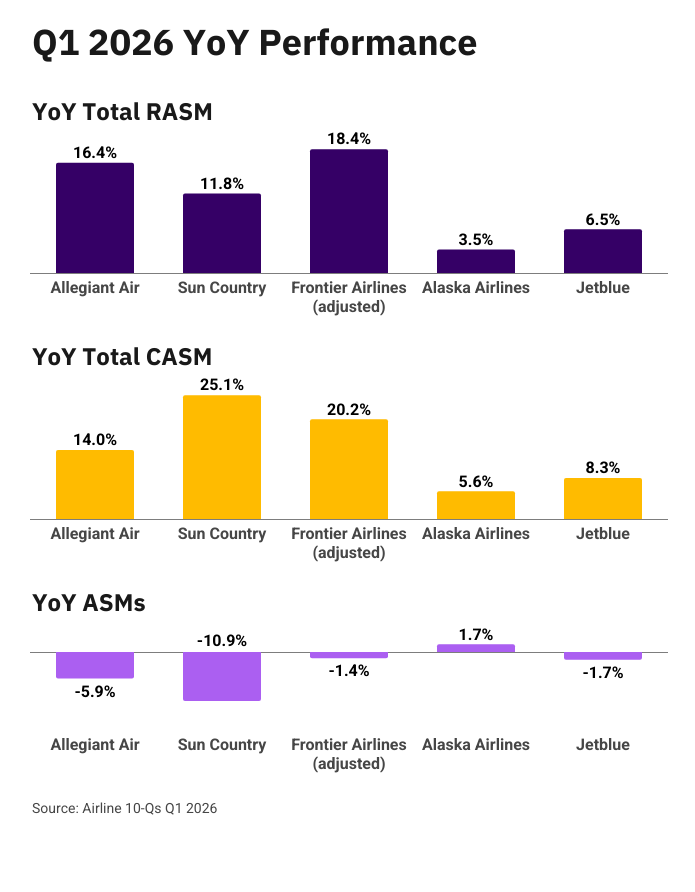

- Unit revenue was a strong point across the board with Allegiant Air, Sun Country and Frontier Airlines all seeing double-digit year-on-year (YoY) RASM growth

- Cost pressures were clearly a challenge, particularly as higher fuel prices hit the spring break peak towards the end of the quarter

Allegiant Air

Allegiant Air delivered the highest quarterly operating margin of all airlines in the US, coming in at 11.1%. Moreover, the airline was the only one of the five mid-size carriers to see better margin performance than last year.

Allegiant Air expects unit revenue growth in the second quarter to exceed the 16.4% posted for the first quarter and commented that “contractual fuel pass-through structures” at Sun Country's cargo and charter businesses would help to offset the impact of higher fuel prices.

Given higher input costs, the airline expects to reduce production by 6.5% YoY in the second quarter "by reducing off-peak capacity" and cutting some "longer stage length routes where the hurdle on fuel cost is higher".

Frontier Airlines

While we would normally report financial results on a GAAP basis, for Frontier Airlines we are using the adjusted metrics to better reflect the underlying performance of the business given the large swings in one-off effects. This strips out the impact of a $139 million charge for early termination of 24 A32neo aircraft and the $73 million TSA reserve.

Frontier Airlines saw the highest uplift in unit revenue among the five airlines with revenue per available seat mile (RASM) up 18.4% on last year. The airline expects a 35-45% recapture rate for higher fuel prices in Q2 and a 3-5% unit revenue uplift as a result of Spirit's shutdown.

Aircraft utilization fell from 9.7 block hours/day in Q1 2025 to 8.5 block hours/day in Q1 2026, which, in addition to a 13% YoY higher fuel cost per gallon, would have put pressure on cost performance.

The 24 A320neo aircraft to be returned to the lessor are due to leave the fleet by June 2026.

Alaska Airlines

Q1 was challenging for Alaska Airlines due to the impact of severe storms in Hawaii and civil unrest in Puerto Vallarta. The two regions make up 30% of the Group's capacity. This resulted in a one point headwind for YoY RASM growth which came in at 3.5% and was the slowest unit revenue growth among all the US airlines.

Premium revenue and managed corporate travel were, however, bright spots for the quarter with revenue up 8% and 19% YoY, respectively.

The airline also noted that both its Seattle-Tokyo and Seattle-Seoul services are operating at load factors above 90% and that the Tokyo service was profitable in March.

JetBlue

As we have covered previously, Fort Lauderdale was a strong performer for JetBlue with unit revenue at the south Florida airport growing 5% YoY despite 23% capacity growth.

JetBlue expects a 30-40% recapture rate for higher fuel prices in Q2, increasing to 100% by early 2027.

As with Alaska Airlines, premium revenue delivered strong performance. Premium cabin RASM grew nine points ahead of Core revenue.

Read our full coverage of JetBlue's Q1 performance.